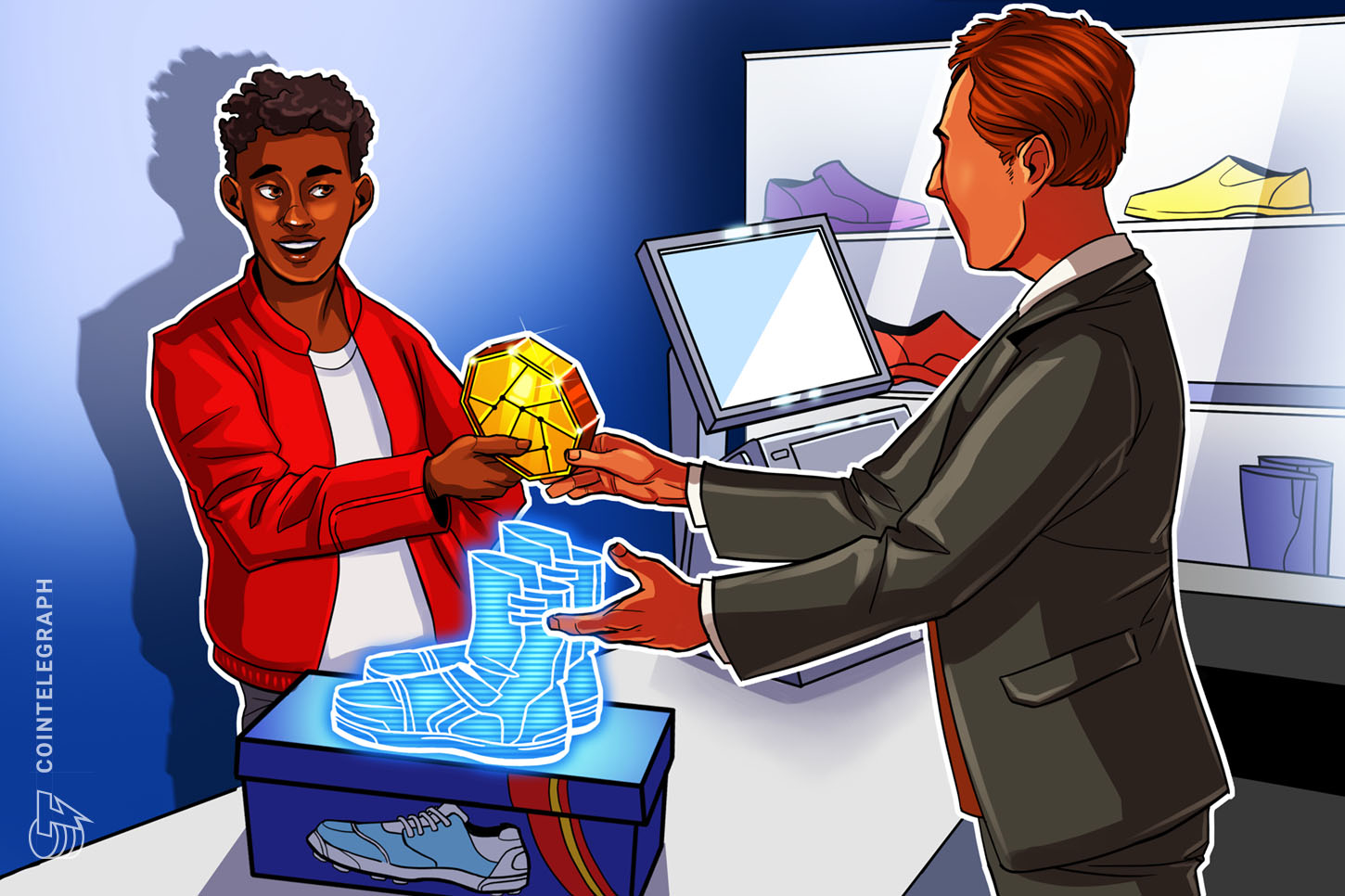

Close your eyes and imagine the future. You walk into a shoe store. You buy a pair of expensive shoes with your favorite cryptocurrency. You did not have to pay the entire cost of the shoes because you had some digital store credit that you had earned by blogging about the business. Now, you own a physical pair of shoes, but the store has also given you a digital token representing your shoes.

It is your lucky day. The digital shoes you just received are ultra-rare. They have platinum laces and are diamond-studded. You just hit a digital lottery! You race home and turn on your game console. You send the digital shoes from your wallet to your game. You find the digital card representing your favorite basketball star, and you equip them with the digital shoes. Boom! Powerup unlocked, and now your sports star runs faster, and the chance of spraining their ankle in the game has reduced.

You play games with your friends, and your powerhouse star helps you to trounce your buddy in Japan. The game sends you some cryptocurrency as a celebratory gift. You post your satisfying victory on social media and earn praise and more crypto for having smashed your friend so brutally.

Welcome to web 3.0.

The status quo — Web 2.0

We’re not there yet. We’re still building the necessary infrastructure, and web 3.0 is worth the wait.

Let’s roll back the clock and talk about now. We walk into a store and buy an item. The cashier hands us a receipt after we pay in cash or card. Or, when we work with a real estate agent and purchase a house, we get a deed. Even if you have to register your motorcycle at the Department of Motor Vehicles, you will be asked to present a vehicle identification number. All of these actions require some form of deed or receipt to track ownership. Nearly all of this is done on paper, but there is a better way to do this tracking by using an open-source and public database that is also known as a blockchain.

If you’ve been living outside the fintech space, you may not have heard of blockchain technology or cryptocurrency. In short, a blockchain is a public and open-source database that stores data over time in chunks (blocks) as it grows.

Cryptocurrencies like Bitcoin (BTC) or Litecoin (LTC) utilize blockchain technology as a stable platform to transact and store the data of transactions. You can download a wallet in order to earn or buy cryptocurrency and send it around the world with near zero barriers. It’s hardcoded economic freedom.

Modern databases are powerful machines capable of doing millions of transactions per second. They can be used for more than just transferring numbers around among users. So, yes, you can send BTC to your sister for her birthday, but there’s more to it.

What’s a nonfungible token?

If I say I’ll give you a dollar, you wouldn’t typically ask me, “Which one?” It doesn’t matter. Any dollar bill with George Washington on it out of my wallet will likely suffice for you to buy something at 7/11. Similarly, if I tell you, “I’ll send you a Bitcoin so you can buy a motorcycle,” you’re not going to ask me, “Which Bitcoin?” While each Bitcoin can, in reality, be tracked separately, the market treats all of them as entirely equivalent, and the buzzword for that is “fungible.”

Imagine it’s our wedding day, and I tell you that I’ve bought you a house. Before getting all excited, you may want to ask, “Which one did you buy?” That’s because all houses aren’t exact replicas of one another. They’re different. And even model homes using the same plans are different because of their construction. Houses are unique; their mortgages are unique, and these are tracked separately with lots of painstaking detail.

Houses, receipts, trading cards and many other things in this world are nonfungible. They are unique; they can’t be substituted even with something that has the same name or shape — for example, an autographed football card or a house whose roof has caved in. There are differences in everything that exists.

On a blockchain, there are generally two types of tokens that can be tracked. Fungible tokens are like currencies that don’t have unique properties, and all we care about is quantity and ownership. Nonfungible tokens, however, differ in that we can track things in detail for property rights, time of purchase, evidence of the transaction, edition, rarity, statistics and millions of other possible categories that make something unique.

NFTs can serve as a digital deed or receipt and then it can have utility. The next time you buy a pack of trading cards, you can pay with crypto and receive NFTs in return.

These tokens can also represent property rights. Imagine that you buy clipart. You can download the images, but if you want to use them commercially, you have to own the token that transfers the rights. If a company sees its image being used, the NFT in your possession indicates that you have purchased the right to use those images.

These tokens can also be used to track individual inventory. You could receive an NFT when you buy a brand new car or a house. The keys to your wallet and the presence of the NFT proves that you are the rightful owner. More importantly, others can use the public database to check if you are the rightful owner. There is no more need to worry about whether something is counterfeit or not. You either have the keys and NFT in your wallet, or you don’t; and anyone with an internet connection can check.

Web 3.0 unlocked

Crypto is a brutal space. One minute, token prices are falling, and the question you ask yourself is: “Can I survive this?” The next minute, prices are climbing, and the question now is: “Can I scale rapidly?” The market is savage. That’s leading to a lot of boom and bust in the market, it’s also creating hardened and sustainable companies. It’s hard to be wasteful on a blockchain as the market chews them up.

The nascent industry is still experiencing growing pains, but distributed blockchains have been developing, and businesses have been increasingly setting themselves up on blockchains. Once they’re established on a blockchain, businesses will be able to track transactions in detail with unique tokens, and those tokens will be transferable across vast interconnected networks.

You’ll get your collectible sports stars, buy digital rights to your favorite piece of art, send your kid crypto on their birthday, and watch as commerce is reshaped by blockchain technology and NFTs. Smile, you are a bitpunk or will be soon enough.

The views, thoughts and opinions expressed here are the authors alone and do not necessarily reflect or represent the views and opinions of Cointelegraph.

This article was co-authored by Aly Madhavji and Jesse Reich.

Aly Madhavji is the managing partner at Blockchain Founders Fund which invests in and builds top-tier venture startups. He is a limited partner on Loyal VC. Aly consults organizations on emerging technologies, such as INSEAD and the United Nations on solutions to help alleviate poverty. He is a senior blockchain fellow at INSEAD and was recognized as a “Blockchain 100” Global Leaders of 2019 by Lattice80. Aly has served on various advisory boards, including the University of Toronto’s Governing Council.

Jesse Reich is the CEO of Splinterlands. Jesse graduated with a Ph.D. in chemistry in four short years and at the age of 27, reached professor status. He spent 10 years as a leading university sales engineer across major corporate publishers. Upon discovering blockchain technology, along with its economic and social liberties, and the protections it offers, Jesse left the publishing sector to found the digital collectibles game Splinterlands with Matt Rosen.